Content

You may use TurboTax Online without charge up to the point you decide to print or electronically file your tax return. Printing or electronically filing your return reflects your satisfaction with TurboTax Online, at which time you will be required to pay or register for the product. In the most common federal audits, taxpayers receive notices from the IRS asking about certain details of their returns and requesting further information or clarification. This is known as a “correspondence audit,” and even those are considered as rare as being struck by lightning. The IRS is on the hunt for taxpayers who sell, receive, trade or otherwise deal in bitcoin or other virtual currency and is using pretty much everything in its arsenal. As part of the IRS’s efforts to clamp down on unreported income from these transactions, revenue agents are mailing letters to people they believe have virtual currency accounts. The agency went to federal court to get names of customers of Coinbase, a virtual currency exchange.

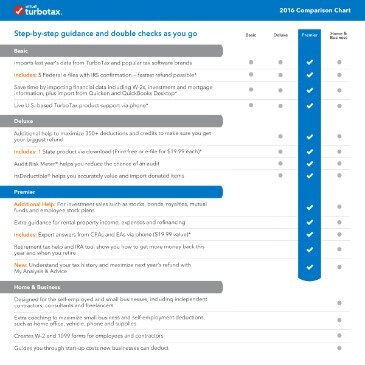

Unusual or unrealistic itemized deductions, either for individuals or small business owners, may raise a red flag for auditors. For example, claiming a charitable tax deduction for 40% of your total income could raise some eyebrows at the IRS. TurboTax helps to make sure your tax return is correct by completing thousands of error checks before you file, so you can be sure it’s accurate. It also features an Audit Risk Meter™ that checks your tax return for common audit triggers and shows you whether your risk is high or low. Learn more about how TurboTax helps you reduce your audit risk.

It’s easy to get deduction-happy when you’re self-employed, since “ordinary and necessary business expenses” are fair game. But realize that the IRS is far stricter about that definition than you may be.

- Additionally, all individual filers must state on page 1 of their 2020 Form 1040 whether they received, sold, sent, acquired or exchanged any financial interest in virtual currency last year.

- Claiming the Earned Income Tax Credit is something of an automatic audit trigger, but you probably won’t even know that the IRS is reviewing your return.

- On Jan. 24, 1986, the IRS received its first electronically filed tax return from a preparer.

- And with TurboTax you can make sure your risk is as low as it can go.

- We’ll search more than 350 tax deductions and credits to find every tax break you qualify for.

Taking a friend out for lunch and trying to pass it off as a business expense? Self-employment itself may not raise your risk of an audit, but it brings a host of opportunities for missteps. Hey, you’re human, and maybe you made a mistake in your math. Perhaps you forgot to fill in some personal information or flubbed a digit in your Social Security number. Unfortunately, whether it’s a simple error or a whopper, it raises your risk of an audit. If the IRS does decide to audit you, there is little you may do to stop it.

Irs Audit Risk No 4: Passing Off A Hobby As A Business

Maurie Backman is a personal finance writer who’s passionate about educating others. Her goal is to make financial topics interesting (because they often aren’t) and she believes that a healthy dose of sarcasm never hurt anyone. In her somewhat limited spare time, she enjoys playing in nature, watching hockey, and curling up with a good book. If your deductions are legitimate, by all means claim them, because you’re entitled to them.

They earn, they pay their bills, and maybe they’re lucky enough to save and invest a little money as well. It can trigger an audit if you’re spending and claiming tax deductions for a significant portion of your income. The majority of audited returns are for taxpayers who earn $500,000 a year or more, and most of them had incomes of over $1 million. These are the only income ranges that were subject to more than a 1% chance of an audit in 2018. The IRS has a computer system called Discriminant Information Function that’s specifically designed to detect anomalies in tax returns. DIF looks for things like duplicate information—maybe two or more people claimed the same dependent—as well as deductions and credits that just don’t make sense. Studies have shown that preparing a tax return and, by extension, risking an IRS audit can actually raise some people’s blood pressure.

If you explain your situation, you may be able to get a refund for the Online product you paid for, but you will have to call – no billing support happens here in the Q&A forum. The regulations demand openness, which in turn increases the likelihood of an audit. That’s because of a perception that taxpayers with foreign accounts are trying to hide income offshore. Audits then occur either by mail or in meetings at taxpayers’ places of business. They can be unpleasant and are sometimes unavoidable. Certain red flags are sure to draw scrutiny and some are easy to sidestep—unreported income, for example.

Turbotax Audit Support Center, Irs Notices, Letters & Tax

That said, some filers are more likely to land on the audit list than others — specifically, those who earn very little or no money, and those who earn a lot. The majority of tax audits aren’t the result of mathematical errors. They occur because something about your financial situation placed you in a category with the IRS that indicates that you might owe more tax dollars than you say you do. And on the bright side, the IRS indicates that nearly 30,000 of the 1 million or so audits conducted in 2018 resulted in the taxpayers getting additional refunds.

Generally speaking, the IRS can be strict about mixing business and personal expenses. Business meals can be allowable, but exceeding the occupational norm by a great amount invites an audit. Business meals oftentimes can be a blurred line, so be sure to document what is and isn’t a personal expense.

Many filers try to claim this lucrative credit even if they’re ineligible. You can check whether you can safely claim the EITC at the IRS website. Taxpayers at the extremes are more likely to attract the attention of the IRS. In 2011, those who made more than $10 million — sorry, Donald Trump — had nearly a 30% chance of being audited.

The ironclad rule is that you must use your home office area for business, and only business. You—and your family members—literally cannot do anything else in that space. Review IRS Publication 587 if you’re planning to claim a deduction for a home office. Presumably, you drove to do personal errands at somepoint. These reporting rules for banking and financial institutions impose time limits as well. A $9,999 deposit on Monday might be reported unless you deposit an additional $1 or more on Tuesday. The IRS says you’re “structuring” your deposit in this case, and there are rules against this, too.

You Have Investment Income

It also wants to make sure that both the payer and the recipient properly reported alimony on their respective returns. A mismatch in reporting by ex-spouses will almost certainly trigger an audit. The IRS is on the prowl for people who receive the advance subsidies and either don’t file returns or file returns but erroneously report the credit. Its computer systems are flagging returns of taxpayers who have modified adjusted gross incomes above the eligible limit to claim the break. Finally, file your taxes electronically rather than on paper. The error rate for electronic returns is less than 1%, but for paper returns, it’s 21%.

Just be prepared to prove and substantiate them if you’re asked. You’re obligated to report all foreign accounts with total cumulative balances of more than $10,000on FinCEN Form 114. Foreign assets valued at $50,000 or more must be reported on IRS Form 8938. You’ll comply with tax law if you do so, but you might also expect the IRS to check and make sure that your account balances really are what you’ve claimed them to be.

That shiny MacBook you bought for personal reasons and only occasionally use for work? Claiming a home office deduction when you use your dining room table as your desk?

Alimony paid pursuant to post-2018 divorce or separation agreements is not deductible (and ex-spouses aren’t taxed on alimony they receive under such agreements). Older divorce pacts can be modified to follow the new tax rules if both parties concur and they modify the agreement in 2019 or later to specifically adopt the tax changes. If the deductions or credits on your return are disproportionately large compared with your income, the IRS may pull want to take a second look at your return. But if you have the proper documentation for your deduction or credit, don’t be afraid to claim it. Don’t ever feel like you have to pay the IRS more tax than you actually owe. These expenses are tallied up on Schedule C and are deducted from your earnings to determine your taxable income from your business.

And with TurboTax you can make sure your risk is as low as it can go. The agency uses occupational codes to measure typical amounts of travel by profession, and a tax return showing 20% or more above the norm might get a second look. The IRS will give a close look to excessive business tax deductions. The IRS will typically receive a copy of all the tax forms that you do, including distributed income. Certain red flags in a tax return are sure to draw scrutiny by the IRS. @0016 I am just a user like you, I have no idea why they took the Audit Mater out of the Online version. Actually the CD/Download version lets you prepare unlimited returns, you get 5 free Federal e-files, there is a charge to e-file a State return.

Your income and financial information has changed this year, however the IRS has looked very closely at 1099-MISC income and deductions for many years. Moving to medium risk does not necessarily mean the IRS will audit your return. If you’re waiting for your tax refund, the IRS has an online tool that lets you track the status of your payment. Additionally, the taxpayer must have a tax home in the foreign country. The tax break doesn’t apply to amounts paid by the U.S. or one of its agencies to its employees who work abroad.

Ditto for business owners who report substantial losses on Schedule C, especially if those losses can offset in whole or in part other income reported on the return, such as wages. On Jan. 24, 1986, the IRS received its first electronically filed tax return from a preparer.

Have you noticed those occupational codes that appear on your tax return? The IRS uses those to make sure that your travel expenditures are in line with others who report those same codes. You’ll most likely get a second look from the IRS if you’ve claimed a lot more than the average for your profession. DIF is on the lookout for deductions that are above the norm for various professions. It might be expected that you would spend 15% or so of your income on travel each year if you’re an art dealer, because that’s about what other art dealers spend. You can probably expect the IRS to take a closer look at your return if you claim 30%. This trigger typically comes into play when taxpayers itemize.

Furthermore, aim to claim deductions that are proportionate to your income — and if they’re not, be prepared with documentation. Additionally, keep accurate records so you know what deductions to claim. Guessing at those numbers, or coming up with remarkably round numbers (like an even $6,000 on medical expenses, for example) is a good way to get your return flagged. Claiming the Earned Income Tax Credit is something of an automatic audit trigger, but you probably won’t even know that the IRS is reviewing your return. The IRS can usually access your account information from a foreign bank, and it will do so if it feels that you might owe taxes on the money you’ve placed there.

With Basic you get Federal only, you would have to purchase a State. If you need to also do a state return Deluxe is the better option. I have never even seen turbo tax offer or advertise the CD/Download.

The IRS wants to be sure that owners of traditional IRAs and participants in 401s and other workplace retirement plans are properly reporting and paying tax on distributions. Special attention is being given to payouts before age 59½, which, unless an exception applies, are subject to a 10% penalty on top of the regular income tax. The IRS hasn’t always been diligent in pursuing individuals who don’t file required tax returns.