Content

MetaBank® does not charge a fee for this service; please see your bank for details on its fees. Severe penalties may be imposed for contributions and distributions not made in accordance with IRS rules. Line balance must be paid down to zero by February 15 each year.

Gains and losses will have the same classification as the underlying property. The income limit for Roth IRA contributions is greatly reduced.

A divorce or separation can be a rough legal and financial process. Luckily, no gain or loss is recognized on allocation of property due to divorce of married couples. For registered domestic partners, however, if there is an unequal division of community property as part of a legal separation, there may be a gain or loss recognized. It is easy to file as Married Filing Separately on eFile.com. Choosing your filing status is one of the first things you do when you start preparing your tax return online.

How A Parent Reports A Child’s Unearned Income

You can file Form 1040X through the H&R Block online and software tax preparation products or by going to your local H&R Block office. What if I receive another tax form after I’ve filed my return? Special rules apply to spouses who live apart for the entire year.

For example, in Balding,29 the taxpayer received payments in settlement of her claim to a community property share of her ex-husband’s military retirement pay. The court held that because the payments were incident to divorce, they should be treated as nontaxable gifts under Sec. 1041. Income from separate property is generally the separate income of the spouse who owns the property. However, in Idaho, Louisiana, Texas, and Wisconsin, income from most separate property is deemed to be community income. Relief from the effects of community property laws is available in certain situations under the innocent spouse provisions in Sec. 6015. for information regarding which income and expenses are considered community property, and which are considered separate property.

But you might not know that community property laws can be extremely important for tax filing, especially if spouses decide to file separate tax returns and they reside in a community property state. In certain states, community property laws can also affect the taxes of a couple in a domestic partnership even though they cannot file as married.

Why Marriage Makes Financial Sense

The information is categorized by tax topic in the order of the IRS Form 1040 or 1040-SR. Apply for an online payment agreement (IRS.gov/OPA) to meet your tax obligation in monthly installments if you can’t pay your taxes in full today. Once you complete the online process, you will receive immediate notification of whether your agreement has been approved. The IRS can’t issue refunds before mid-February 2020 for returns that claimed the EIC or the ACTC. This applies to the entire refund, not just the portion associated with these credits.

Do not combine your separate investment income. Report your entire separate investment income on your own return.

Dividends, interest, and rents from separate property are characterized in accordance with the discussion under Income from separate property, later. For federal tax purposes, marriages of couples of the same sex are treated the same as marriages of couples of the opposite sex. For federal tax purposes, the term “spouse” means an individual lawfully married to another individual and includes an individual married to a person of the same sex.

- Additionally, with the exception of child support payments, neither of you can have shared any of your separate income with the other or with the marital community.

- However, because John chose to continue working until 2002 and did not terminate his participation in the plan following divorce, the pension administrator did not begin making distributions right away.

- In that case, the spouse filing as head of household may be entitled to the EIC.

- In most cases, income from separate property will be separate income that is considered to belong to the spouse who owns the property.

- The Internal Revenue Service doesn’t recognize registered domestic partnerships as marriages for federal tax purposes.

Wages, salaries, and other compensation your spouse received for services he or she performed as an employee. You may be entitled to a credit for other dependents for each qualifying child who isn’t a qualifying child for the child tax credit and for each qualifying relative. For more information, see the instructions for your return. For specific information that pertains to your situation, check with the laws of your state. A registered domestic partner may itemize or claim the standard deduction regardless of whether his or her partner itemizes or claims the standard deduction. Descriptions of registered domestic partnerships and related topics have been included in the relevant sections. Each week, Zack’s e-newsletter will address topics such as retirement, savings, loans, mortgages, tax and investment strategies, and more.

For example, if Mary will have her refund garnished to pay student loan debt, her wife, Nancy, may want to file a separate return to receive her share of the refund. The whole joint refund would be subject to Mary’s obligation if a joint return was filed. Depending on the specific state law, this strategy may or may not work in a community property state. In some states, community property is subject to premarital and separate debts either spouse. In these states, the full joint overpayment can be garnished to fulfill Mary’s obligation.

If H&R Block makes an error on your return, we’ll pay resulting penalties and interest. Enrolled Agents do not provide legal representation; signed Power of Attorney required.

Disadvantages Of Filing Separate Returns

If you lived with your spouse at any time during the year, you cannot deduct a loss from passive rental real estate activity. If you did not live together, you can claim this deduction, but the amount will be limited. You cannot exclude any interest income from U.S. savings bonds that you used for education expenses. You will generally have a higher tax rate than you would have on a joint return. If your spouse itemizes deductions, you cannot claim the standard deduction.

W’s IRA was classified as her individual property. The balance of H’s IRAs would then be classified as his individual property under state law and the marital property agreement. Before the divorce court could act, Hazel and Joe settled with regard to the retirement pay. Hazel relinquished any claim to Joe’s military retirement pay in consideration of Joe’s promise to pay to her $15,000, $14,000, and $13,000 in 1986, 1987, and 1988, respectively. Hazel did not include the settlement payments in her original returns for the years in question. After she received a private letter ruling concluding that the settlement payments were includible, she fi led amended returns including the income and then challenged the IRS’s determination in Tax Court. Enrollment in, or completion of, the H&R Block Income Tax Course is neither an offer nor a guarantee of employment.

Download the official IRS2Go app to your mobile device to check your refund status. If your SSN has been lost or stolen or you suspect you’re a victim of tax-related identity theft, visit IRS.gov/IdentityTheft to learn what steps you should take. The IRS doesn’t initiate contact with taxpayers by email or telephone to request personal or financial information. This includes any type of electronic communication, such as text messages and social media channels.

Beverly Bird has been writing professionally for over 30 years. She specializes in personal finance and w, bankruptcy, and she writes as the tax expert for The Balance. The Uniform Premarital and Marital Agreements Act allows parties to a prenup to choose the financial terms of their marriage.

You may have a smaller child tax credit and credit for other dependents than you would on a joint return. You can’t take the credit for the elderly or the disabled unless you lived apart from your spouse all year. You can’t exclude any interest income from qualified U.S. savings bonds that you used for higher education expenses. Treat social security and equivalent railroad retirement benefits as the income of the spouse who receives the benefits. Earned income doesn’t include amounts paid by a corporation that are a distribution of earnings and profits rather than a reasonable allowance for personal services rendered. Your spouse’s (or former spouse’s) distributive share of partnership income. Income your spouse derived from a trade or business he or she operated as a sole proprietor.

A married taxpayer who files a joint return may avoid unfair tax consequences through the innocent spouse provisions of Sec. 6015. In 1980, Congress enacted Sec. 66 to provide relief to married taxpayers domiciled in a community property state who file separate returns and who without such relief would suffer inequitable tax treatment. Sec. 66 has since been expanded and modified several times. A registered domestic partner must report half of all community income and all of his or her separate income unless certain exceptions apply. Generally, the laws of the state in which the registered domestic partnership is domiciled governs whether the RDP has community income or separate income. Community property, generally, includes earned income, self-employment income from sole proprietorships, interest, dividends, and rent.

Community property is a state-level legal distinction of a married person’s assets, such as property acquired during the course of a marriage. The great majority of states—41, to be exact—rely on the concept of common law property to determine who owns property that is acquired during a marriage. Responsibility for any debts that date from before the marriage is not shared. And if you purchased property with a combination of community and individual funds, only the part bought with community funds is considered shared. The property to be divided does not include assets owned by either spouse prior to the marriage or after a legal separation. Gifts or inheritances received by one spouse during the marriage are also excluded. In certain states the community can be ended through separation of the spouses without the need for a formal agreement.

How To Deduct Property Taxes On A Home Based Business

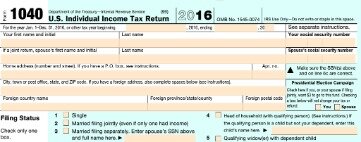

Broadly speaking, a divorce court in a community property state will split all other assets 50/50 unless both parties agree on another arrangement. In many cases, this requires that any joint property be sold so that the former partners can split the proceeds. Only nine states are classified as community property states, but state laws vary; some lean more toward the community property standard, and others abide by a common law standard. Divorce laws vary by state, with some leaning more toward the community property concept. But these nine states are the only true community property states as of late 2020. This is where they will list the spouse’s return information. For Registered Domestic Partners you would fill out your federal returns separately and then combine your information on the state return only.

This publication is also for registered domestic partners who are domiciled in Nevada, Washington, or California. Registered domestic partners in Nevada, Washington, or California generally must follow state community property laws and report half the combined community income of the individual and his or her registered domestic partner. If you’re married/Registered Domestic Partner , you may choose to file separately. Each spouse or partner will prepare a separate tax return and report their individual income and deductions. Valid for 2017 personal income tax return only. Return must be filed January 5 – February 28, 2018 at participating offices to qualify.

The same reporting rule applies to registered domestic partners. For a discussion of the effect of community property laws on certain items of income, deductions, credits, and other return amounts, see Identifying Income, Deductions, and Credits, earlier. When a married couple chooses to file separate tax returns, sometimes no one gets the credit. Under this filing status, there are limits on the tax credits you can take, regardless of whether you are domiciled in a community property state. The married filing separate status disqualifies you from claiming the earned income tax credit, the credit for child and dependent care expenses, the adoption credit, and any educational credits. There are situations in which a separated spouse might suffer an unfair income tax result if the community property laws were applied.