Small or private companies may also use financial accounting, but they often operate with different reporting requirements. Financial statements generated through financial accounting are used by many parties outside of a company, including lenders, government agencies, auditors, insurance agencies, and investors. An income statement can be useful to management, but managerial accounting gives a company better insight into production and pricing strategies compared with financial accounting. Financial accounting rules regarding an income statement are more useful for investors seeking to gauge a company’s profitability and external parties looking to assess the risk or consistency of operations. Just as managerial accounting helps businesses make decisions about management, cost accounting helps businesses make decisions about costing. Essentially, cost accounting considers all of the costs related to producing a product.

The purpose of financial accounting is to offer accountability and transparency. Financial accounting ensures that management is answerable for their financial actions and results. In contrast, managerial accounting guides internal users, such as management, in making operational decisions. As per this concept, each business transaction has a dual or a two way effect. This is to say every amount debited in a transaction must be equal to every amount credited in that transaction.

Accrual Accounting

Financing expenses refer to expenses relating to non-equity financing used to raise capital for the business. And capital expenses are the ones that generate benefits over long periods of time. This concept of accounting states that expenses incurred in a particular accounting period should match with the revenues generated during the same period. So, to take important financial decisions, a business owner needs to maintain proper financial statements. This is to bring uniformity across the financial statements of entities of the specific region/country and undertake inter company comparisons easily.

- In the ever-evolving business world, adherence to these principles and standards ensures a level playing field for companies, lenders, investors, and regulators, wherever they may be.

- The goal is to meet our expectations when we interpret financial statements.

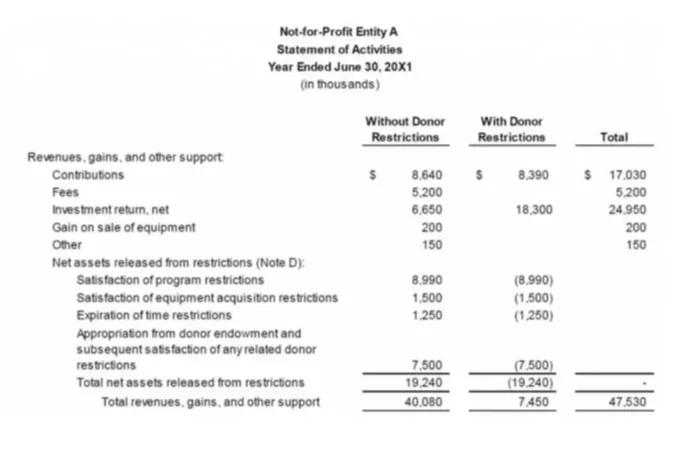

- The financial statements used in accounting are a concise summary of financial transactions over an accounting period, summarizing a company’s operations, financial position, and cash flows.

- For example, a goods manufacturer will have a variety of sales and payment categories.

These statements provide a snapshot of the company’s financial position and performance during the accounting period. Financial statement reporting includes the balance sheet, income statement, and cash flow statement. Accountants help businesses maintain accurate and timely records of their finances. Accountants also provide other services, such as performing periodic audits or preparing ad-hoc management reports. Accounting is the process of recording financial transactions pertaining to a business.

Unlocking the Power of Financial Accounting: Illuminating the Beneficiaries

Under accrual accounting, the company is not allowed to recognize the $1,000 as revenue, as it has technically not yet performed the work and earned the income. The transaction is recorded as a debit to cash and a credit to unearned revenue, a liability account. When the company earns the revenue next month, it clears the unearned revenue credit and records actual revenue, erasing the debt to cash.

The Alliance for Responsible Professional Licensing (ARPL) was formed in August 2019 in response to a series of state deregulatory proposals making the requirements to become a CPA more lenient. The ARPL is a coalition of various advanced professional groups including engineers, accountants, and architects. Accounting history dates back to ancient civilizations in Mesopotamia, Egypt, and Babylon.

Principles of Financial Accounting

Furthermore, transactions are recorded in terms of monetary units and not in terms of units of physical quantity. Transactions or happenings that cannot be expressed in monetary terms are not recorded in accounting statements. Typically, a business would realize revenues at the time of selling goods or rendering of services. This means that a business would realize revenues only when the legal right to receive such revenues arise. As per this concept, revenues arising on account of sale of goods or services rendered must be recorded only when they are realized. However, all losses, including the ones that have less chances of occurring, should be recorded in the books of accounts.

- Financial accounting ensures that management is answerable for their financial actions and results.

- At the heart of a company’s operations, management generates and relies on financial accounting to make informed decisions.

- Managerial accounting also encompasses many other facets of accounting, including budgeting, forecasting, and various financial analysis tools.

- Generally Accepted Accounting Principles (GAAP) is the standard framework of guidelines for financial accounting used in any given jurisdiction.

Financial accounting is a specific branch of accounting involving a process of recording, summarizing, and reporting the myriad of transactions resulting from business operations over a period of time. In most cases, accountants use generally accepted accounting principles (GAAP) when preparing financial statements in the U.S. GAAP is a set of standards and principles designed to improve the comparability and consistency of financial reporting across industries. Periodically, usually at the end of a financial period, financial transactions are summarized into quarterly or annual financial statements.

Professional Designations for Financial Accounting

This means that assets need to be recorded at their purchase price in books of accounts. Such a price includes the cost of (i) acquisition, (ii) transportation, (iii) installation and (iv) making the asset ready to use. Now, every business needs to maintain such accounting records so that the income or loss as well as the financial position data can be communicated to all the stakeholders of the business. The Securities and Exchange Commission has an entire financial reporting manual outlining reporting requirements of public companies.

In short, although accounting is sometimes overlooked, it is absolutely critical for the smooth functioning of modern finance. The difference between these two accounting methods is the treatment of accruals. Tax accountants overseeing returns in the United States rely on guidance from the Internal Revenue Service. Federal tax returns must comply with tax guidance outlined by the Internal Revenue Code (IRC). Tax accounts may also lean in on state or county taxes as outlined by the jurisdiction in which the business conducts business. Foreign companies must comply with tax guidance in the countries in which it must file a return.