Accurate accounting helps in valuing these reserves, determining depletion, and providing insights into the company’s overall asset base, influencing strategic decisions and financial planning. The process of calculating DD&A involves several steps, starting with the estimation of the total recoverable reserves for depletion purposes. This estimation is crucial as it directly impacts the rate at which costs are allocated over the productive life of the asset. Companies often use advanced software like PHDWin or ARIES to model these calculations, ensuring precision and compliance with industry standards. For depreciation and amortization, companies must determine the useful life of the asset and select an appropriate method, such as straight-line or units-of-production, to allocate costs systematically over time.

Oil and gas accounting, financial reporting, and tax update

Accounting methods and principles should be applied consistently from one period to another. Expenses should be recognized in the period in which they are incurred, helping to match costs with the revenue they generate. However, when there are no new reserves added, each company’s CFO will be the same. This is because adding back the non-cash charge for DD&A effectively negates the relatively larger impact to net income under the FC accounting method.

Hierarchy of Accounting Principles

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the “Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of public accounting.

COPAS Epublications Library & Subscription

The standard outlines a single comprehensive model for entities to use in accounting for revenue. This section dives into the changes in the key accounting issues due to the new revenue recognition standard. Exact accounting data is critical for evaluating project economics, making informed investment decisions, and planning for the future. It enables companies to assess project viability, allocate resources efficiently, and make strategic decisions that contribute to long-term success in the industry. The principle outlines when and how to recognize revenue from the sale of goods or services. It provides guidance on the recognition criteria, measurement, and disclosure of revenue in financial statements.

- It ensures that financial information is accurate, transparent, and aligned with industry standards, contributing to the overall integrity and sustainability of the oil and gas sector.

- When there are conflicts between different accounting principles or methods, a hierarchy exists to guide the selection of the most appropriate principle.

- Generally accepted accounting principles (GAAP) require that companies charge costs to acquire those assets against revenues as they use the assets.

- In the oil and gas sector, this can occur at different stages, such as at the wellhead, after transportation, or upon delivery to a refinery.

- When it comes to oil and gas companies, everything revolves around how they treat capitalized costs.

- COPAS Energy Education runs a number of open enrollment classroom classes throughout the year in major centers of the industry including Houston, Dallas, and Fort Worth in Texas; Denver, Colorado; and Oklahoma City, Oklahoma.

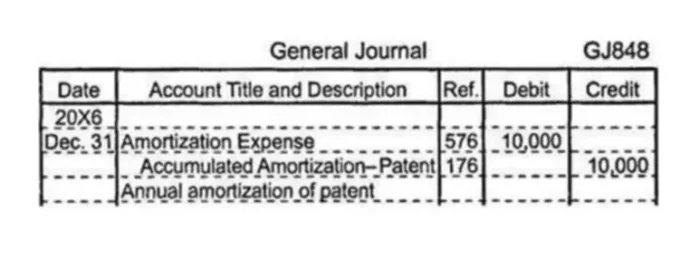

Accounting for Depletion, Depreciation, and Amortization (DD&A)

Other costs, such as geological and geophysical costs, are mostly expensed as incurred. Regardless of industry, all publicly traded companies in the United States follow accounting principles set forth by U.S. As oil and gas reserves are extracted, companies need to allocate the costs of acquiring and developing these reserves over time. DD&A is the accounting method used to spread these costs over the life of the reserves. However, without the subsequent discovery of new reserves, the resulting decline in periodic production rates will later begin to negatively impact revenues and the calculation of DD&A for both a SE and FC company. Revenue recognition in the oil and gas industry is a complex process influenced by various factors, including the nature of contracts, the timing of delivery, and market conditions.

When it comes to oil and gas companies, everything revolves around how they treat capitalized costs. You must possess a deep breadth of knowledge about contemporary financial techniques and how they apply to the energy industry. COPAS Energy Education runs a number of open enrollment classroom classes throughout the year in major centers of the industry including Houston, Dallas, and Fort Worth in Texas; Denver, Colorado; and Oklahoma City, Oklahoma. We also provide our set classes, or customized education days for our COPAS societies and private companies at affordable rates upon request.

Variable consideration can include price adjustments based on market conditions, volume discounts, or performance bonuses. Companies must estimate the amount of variable consideration they expect to receive and include it in the transaction price. This estimation process involves significant judgment and can impact the timing and amount of revenue recognized. Advanced software tools like SAP S/4HANA and Oracle’s Oil and Gas Accounting solutions are often employed to manage these complexities, providing real-time data and analytics to support accurate revenue recognition. Production costs, also known as lifting costs, are the expenses related to extracting oil and gas from the ground and bringing it to the surface.

Most major E&P companies implement the Successful Efforts (SE) method due to the transparency it provides. In SE, costs are capitalized based on whether the well is successful or not (i.e., hydrocarbons are produced). If it’s unsuccessful, the costs are immediately expensed to the income statement.

Companies record exploration costs capitalized under either method on the balance sheet as part of their long-term assets. This is because, like the machinery used by a manufacturing company, oil and natural gas reserves are considered productive assets for an oil and gas company. Generally accepted accounting principles (GAAP) require that companies charge costs to acquire those assets against revenues as they use the assets. Oil and gas accounting is a specialized discipline essential for accurately tracking and reporting financial activities in the oil and gas industry.

We are committed to delivering the highest quality, lifelong, learning experience to accounting professionals in the oil and gas industry. As a COPAS member, you are at the forefront of driving change and innovations that shape accounting in the petroleum industry. Here, you can access your account, membership details, and other important information. Being a COPAS member means that you are at the forefront of driving change and innovations that shape accounting in the petroleum industry. If your company is on the lookout for high-quality oil and gas accountants, talk to EAG Inc..

It ensures transparent financial reporting, compliance with regulations, and strategic decision-making. As an intricate discipline, oil and gas accounting plays a pivotal role in valuing assets, managing risks, and supporting sustainable practices in the exploration, extraction, and production of oil and gas resources. In addition to these factors, companies must also consider the impact of joint ventures and partnerships on revenue recognition.

However, such a comparison also points out the impact on periodic results caused by differing levels of capitalized assets under the two accounting methods. One of the primary considerations in revenue recognition is the point at which control of the product is transferred to the customer. In the oil and gas sector, this can occur at different stages, such as at the wellhead, after transportation, or upon delivery to a refinery. The terms of the contract will dictate the specific point of transfer, which in turn determines when revenue can be recognized. For instance, a contract might stipulate that revenue is recognized when the oil is delivered to a storage facility, rather than when it is extracted from the ground. This distinction is crucial for accurate financial reporting and compliance with accounting standards.

These requirements vary widely from state to state, and it’s important to have a system that can support these requirements and make compliance a breeze. The theory behind the FC method holds that, in general, the dominant activity of an oil and gas company is simply the exploration and development of oil and gas reserves. Therefore, companies should capitalize all costs they incur in pursuit of that activity and then write them off over the course of a full operating cycle. Asset Retirement Obligations (AROs) represent a significant aspect of financial planning and reporting in the oil and gas industry.