Content

ISO holders will report nothing at this point; no tax reporting of any kind is made until the stock is sold. If the stock sale is a qualifying transaction, then the employee will only report a short-term or long-term capital gain on the sale. If the sale is a disqualifying disposition, then the employee will have to report any bargain element from the exercise as earned income. ISOs resemble non-statutory options in that they can be exercised in several different ways. The employee can pay cash upfront to exercise them, or they can be exercised in a cashless transaction or by using astock swap. The profits on the sale of NSOs may be taxed as ordinary income or as some combination of ordinary income and capital gains, depending on how soon they are sold after the options are exercised.

This discount on the purchase price of the stock is called the spread. Janet Berry-Johnson is a CPA with 10 years of experience in public accounting and writes about income taxes and small business accounting for companies such as Forbes and Credit Karma. Individuals with high ordinary income, such as wages, could be even further immunized from the AMT regime. deferral of income tax consequences will not be an available choice. You may use TurboTax Online without charge up to the point you decide to print or electronically file your tax return. Printing or electronically filing your return reflects your satisfaction with TurboTax Online, at which time you will be required to pay or register for the product.

The value of ISOs becoming exercisable for the first time in any calendar year cannot exceed $100,000. A strategic approach that considers factors like your cash flow, tax implications and overall portfolio diversification will give you the best chance of seeing the benefit of ISOs.

ISOs have a strike price, which is the price a holder must pay to purchase one share of the stock. ISOs may be issued both by public companies and private companies, with ISOs being common as a form of executive compensation for public companies, and common as a form of equity compensation in private start-up companies. Sometimes, companies offer stock as part of your employee compensation package. They usually issue incentive stock options , non-qualified stock options , or restricted stock units .

Why Are Incentive Stock Options More Favorable Tax

When planning for your final sale of stock, it is important to understand what other income you have and how much room you have in various capital gains tax brackets. If you don’t meet the requirements you have a disqualifying disposition and the bargain element will be taxed as ordinary income. It won’t be subject to Social Security and Medicare wage tax (I point this out as a difference between NSOs and ISOs. NSOs are subject to Social Security and Medicare wage tax). ISOs have a special holding period to qualify for capital gains tax treatment. The holding period is two years from the grant date, and one year after the stock was transferred to the employee.

Selling to cover exercise costs is called a “cashless” exercise. However, selling shares right after exercising prevents you from taking advantage of ISOs’ favorable tax structure. Not all companies allow cashless exercises, so check to see if yours does before exercising and check with your tax advisor in general. Even if your company gives you a long time to exercise ISOs after you leave, if you don’t exercise them within three months of leaving, they’ll lose their ISO tax treatment and will be taxed like NSOs.

Stock options give holders the right to buy or sell a certain security at a certain price for a certain period of time. You can buy and sell stock options on thousands of publicly traded stocks through a typical brokerage account. Incentive stock options are the same basic contract, where you’re given the right to buy a certain number of shares of your company for a specific dollar amount. Now, what happens if you exercise and receive shares, then sell prior to achieving qualified disposition status on those shares?

Statutory Stock Options

The later in the year he exercises, the greater the risk that in the following tax year the price of the stock will fall precipitously. If John waits until after December 31 to sell his shares, but sells them before a one-year holding period is up, then things are really bleak. He is still subject to the AMT and has to pay ordinary income tax on the spread as well.

Complete a separate Schedule D and Form 8949 to report the different AMT gain. Use Form 6251 to report a negative adjustment for the difference between the AMT gain and the regular capital gain. For disqualifying dispositions of ISO shares, the cost basis will be the strike price—found on Form 3921—plus any compensation income reported as wages. This inclusion of the ISO spread in AMT income only triggers if the employee continues to hold the stock at the end of the same year in which the option was exercised. If the stock is sold within the same year as its exercise, then the spread does not need to be included in AMT income.

![]()

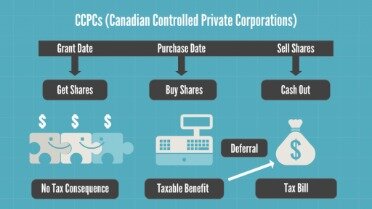

For regular tax purposes, the cost basis of the ISO shares is the price paid—the exercise or strike price. For AMT purposes, the cost basis is the strike price plus the AMT adjustment—the amount reported on Form 6251, line 2i. Stock can be purchased at the strike price as soon as the option vests . Strike prices are set at the time the options are granted, but the options usually vest over time. If the stock increases in value, the ISO allows the employee to purchase stock in the future at the previously locked-in strike price.

Requirements For Classification As Iso

There are several types of stock purchase plans that contain these features, such as non-qualified stock option plans. These plans are usually offered to all employees at a company, from top executives down to the custodial staff. For the employee, the downside of the ISO is the greater risk created by the waiting period before the options can be sold. In addition, there is some risk of making a big enough profit from the sale of ISOs to trigger the federal alternative minimum tax . That usually applies only to people with very high incomes and very substantial options awards. Say a company grants 100 shares of ISOs to an employee on December 1, 2019. The employee may exercise the option, or buy the 100 shares, after December 1, 2021.

This usually means you pay more taxes with NSOs than with ISOs. A non-open market describes a private agreement to purchase or sell shares directly from a company without the use of a market exchange.

Like the strategy discussed in the NQSO planning section, this can be used to improve cash flow during the exercise event. The immediate sale of the shares to cover the AMT is a disqualifying disposition. The remaining shares received can be held for future appreciation and, if the holding period requirements are met, favorable qualifying disposition treatment. Further, since ISOs do come with such potentially lucrative benefits, it’s possible for employees to stock up (no pun intended!) on company shares. Note that both the exercise date and the final sale date are different than those used to illustrate a qualifying disposition. In this example, we meet the first test for a qualifying disposition because the final sale date was more than two years from the grant date.

- Incentive stock options are similar to non-statutory options in terms of form and structure.

- The name of the game is waiting, and how long you wait to sell your shares will determine if you trigger a qualifying or disqualifying disposition.

- Theoretically, ISOs expire 10 years from the date you’re granted them.

- In essence, when ISOs and when non-qualified options are recognized are reversed in the two tax systems.

- IRS Form 6251, will have a negative adjustment on line 2k to reflect the difference in gain or loss between the regular and AMT gain calculations.

A qualified employee stock option is known as a statutory stock option and offers an additional tax advantage for the holder. Outside of taxation, ISOs feature an aspect of what is called discrimination. Whereas most other types of employee stock purchase plans must be offered to all employees of a company who meet certain minimal requirements, ISOs are usually only offered to executives and/or key employees of a company. ISOs can be informally likened to non-qualified retirement plans, which are also typically geared toward those at the top of the corporate structure, as opposed to qualified plans, which must be offered to all employees.

This will somewhat minimize capital outlay while allowing for the potential capture of future growth in the stock’s value. If you fail to fulfill either of the waiting period requirements for a qualified disposition, then you have a disqualifying disposition and you lose the tax advantage of long-term capital gains rates.

Incentive Stock Options (isos)

Given this, by executing disqualified dispositions of ISO shares, you will likely lower your overall tax liability. Incentive stock options can provide substantial income to its holders, but the tax rules for their exercise and sale can be complex in some cases.

Qualifying disposition refers to a sale, transfer, or exchange of stock that qualifies for favorable tax treatment. ISOs must be held for more than one year from the date of exercise and two years from the time of the grant to qualify for more favorable tax treatment. Other employers use thegraded vestingschedule, which allows employees to become invested in one-fifth of the options granted each year, starting in the second year from the grant. The employee is then fully vested in all of the options in the sixth year from the grant. ISOs are usually issued by publicly-traded companies, or private companies planning to go public at a future date, and require a plan document that clearly outlines how many options are to be given to which employees. Those employees must exercise their options within 10 years of receiving them. ISOs often have more favorable tax treatment on profits than other types of employee stock purchase plans.

If you don’t exercise them before that period ends or before they expire, you’ll lose the opportunity to purchase them. ISOs are a type of stock option that qualifies for special tax treatment.